Who is a Casually Taxable Person - Goods and Services Tax

Join Our Whatsapp Broadcast to Receive Updates On Mutual Funds. Click : Taxationwealth/join

Casual Taxable Person - Overview

A registration under goods and services tax done for a casually taxable person without any permanent place of business in a taxable territory according to GST law is compulsory other than in case of specified handicraft goods who only have to register when aggregate turnover is more than 20 crores and in some states even 10 crores.

For a casually taxable person getting a composition GST number is not an option and even the registration as casually taxable person has to be done 5 days prior to the day when business has to commence.

For a normal individual no registration is required until the aggregate turnover reaches Rs 40 crore but for a casual taxpayer registration is compulsory other than individuals dealing in specified handicraft goods.

If we talk about differentiation among regular and casual tax payer registration then the biggest point can be the advance amount of estimated tax that a casual tax payer has to deposit before hand.

Applicability for Casual Taxpayer Registration

Business is undertaken occasionally and not on regular basis.

Supply of goods and services is done either by principle, agent or in any other capacity.

Business is done in a state or union territory where the taxpayer has no fixed place of business no matter if he has a fixed place set up in some other state.

Registration Process for a Casually Taxable Person

Below are all the steps that are required to be fulfilled for getting registration under goods and services tax.

1. Registration form 'GST REG-01' to be used in regular registration is also used for CTP registration.

2. Disclosure of information like details of PAN, email address, mobile number, bank details, partnership deed if any, existing GST registration if any, nature of business, etc in part A of form GST REG-01which are validated by central board of direct taxes.

3. A temporary reference number also known as TRN is generated and using the same part two of GSTR REG-01 is filed with respective documents and verification is done afterwards.

4. The registration certificate is only issued after the advance tax is deposited with the help of the reference number issued.

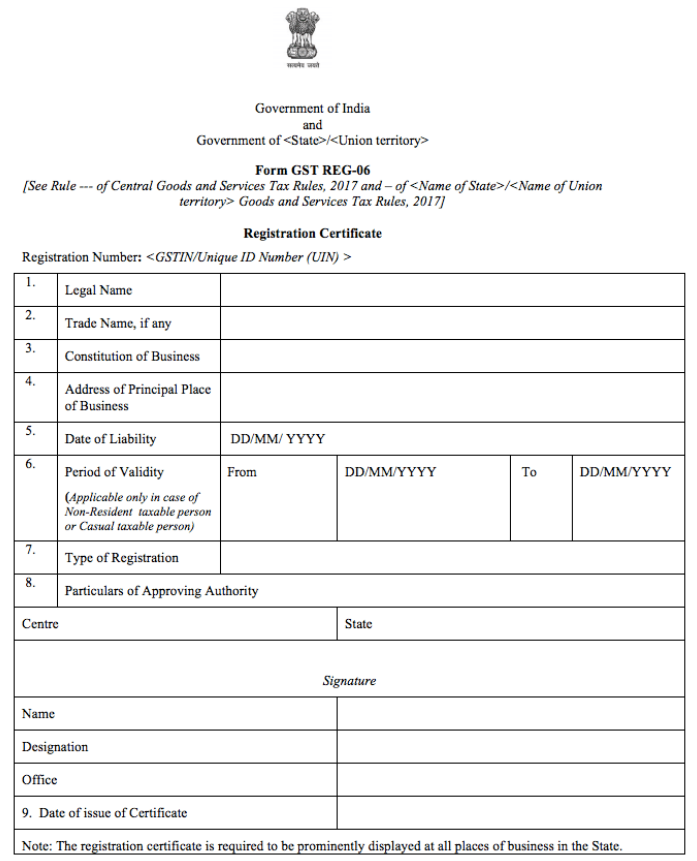

The validity of registration such issued is of 90 days or earlier if mentioned in the application beforehand and an extension in the latter case can be applied through GST REG-11 but only after additional payment is made for estimated advance tax. Below is a sample certificate showing validity details only mentioned in case of casually taxable person.

Return Filing Requirements

For ensuring ethical business practices government has laid down some data gathering practices for every person registered under Goods and Services Tax. And these involve furnishing timely returns such as GSTR-1, GSTR-2, GSTR-3 & GSTR-3B in case of casually taxable person. And their is no need of filing annual GST return.

But currently a CTP is only liable to file the below two returns.

RETURNS

GSTR-1

Outward taxable supply details to be filed before 10th of the next month.

GSTR-3B

Inward taxable supply details to be filed before 20th of the next month.

Since in case of a CTP the GST is estimated and deposited in advance so in case of any balance left in the electronic cash ledger the refund can only be claimed after filing all the due returns.

If you like this post, please do share it with others and also use the below form to Subscribe to our FREE Email Newsletter.

Gourav Ahuja

Hi, i am a gamer. I play with words. I believe in persistence no matter how hard or cumbersome the path of perfection may be and due to this constant urge of achieving what i want people often think me to be abnormal but according to me i just don’t get embarrassed easily since i am already maxed out.